Why Retail Revenue Is Often an Estimate Rather Than a Fact

Why This Matters

In Part 2, we concluded that retail revenue is generally recognised when control transfers to the end consumer.

At first glance, that appears to solve the revenue recognition problem.

A customer purchases a product.

The company recognises revenue.

End of story.

Unfortunately, retail accounting is rarely that simple.

When a customer buys a product, the amount collected today may not ultimately represent the amount the company keeps.

The customer may:

- Return the product

- Use a coupon

- Earn loyalty points

- Receive a rebate

- Redeem a gift card

As a result, retail companies often do not know the final amount of revenue at the moment of sale.

Revenue therefore becomes an estimation exercise.

This is the world of variable consideration.

When Revenue Is Not Fixed

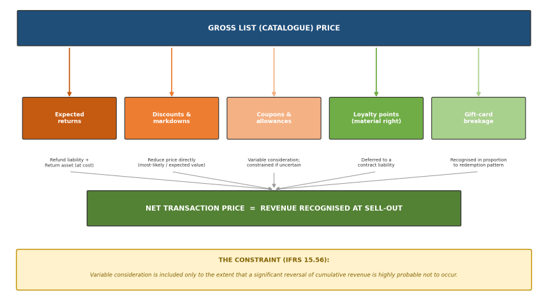

IFRS 15 requires companies to estimate the amount of consideration they expect to be entitled to receive.

In other words, revenue is not necessarily based on the sticker price.

It is based on the amount the company ultimately expects to keep.

Consider a simple example.

A retailer sells products worth $1,000,000 during December.

Historically, approximately 10% of sales are returned during January.

Should the company recognise:

- $1,000,000 revenue?

- $900,000 revenue?

IFRS 15 generally requires management to consider expected returns at the time revenue is recognised.

The result is that revenue becomes an estimate rather than a known fact.

The Variable Consideration Framework

Common Sources of Variable Consideration in Retail

| Item | Common Retail Example |

|---|---|

| Product Returns | Customer returns purchased goods |

| Coupons | Promotional discount coupons |

| Rebates | Volume-based customer incentives |

| Loyalty Programmes | Membership points |

| Gift Cards | Future redemption rights |

| Price Protection | Future selling price adjustments |

Figure 1. Retail companies frequently encounter situations where the final transaction price differs from the original selling price.

The more promotional activity a retailer conducts, the greater the role of estimation in revenue accounting.

Estimating Variable Consideration

IFRS 15 allows two estimation approaches.

Estimation Methods Under IFRS 15

| Method | Description | Typical Use |

|---|---|---|

| Expected Value | Probability-weighted outcome | Large populations of transactions |

| Most Likely Amount | Single most probable outcome | Binary outcomes |

For most retail businesses, the expected value method is usually more appropriate.

Why?

Because retailers process thousands or millions of transactions every year.

Individual customer behavior is unpredictable.

However, the overall population tends to behave predictably.

For example:

- Historical return rate = 8%

- Historical coupon usage = 15%

- Historical gift card redemption = 92%

These patterns allow management to estimate future outcomes with reasonable accuracy.

The Constraint Principle

Estimating revenue is one thing.

Overestimating revenue is another.

To prevent overly optimistic revenue recognition, IFRS 15 introduces a safeguard known as the constraint.

The Variable Consideration Constraint

| Question | Requirement |

|---|---|

| Can revenue be estimated? | Yes |

| Can all estimated revenue be recognised? | Not necessarily |

| What is the limitation? | Revenue must not be subject to a significant future reversal |

In practical terms:

Companies should not recognise revenue today if there is a significant risk that the revenue will need to be reversed tomorrow.

This principle introduces a conservative bias into the accounting model.

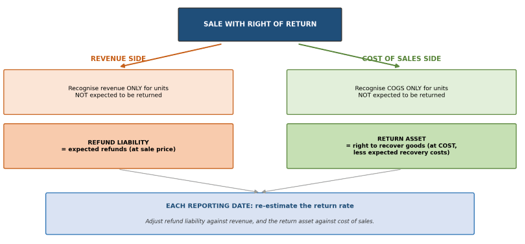

The Right of Return

Returns are one of the most common forms of variable consideration in retail.

A customer purchases a product today but retains the right to return it later.

From an accounting perspective, this creates two questions:

- How much revenue should be recognised?

- What happens if the product comes back?

IFRS 15 answers these questions using a dual-accounting approach.

Accounting for Expected Returns

| Element | Accounting Treatment |

|---|---|

| Revenue | Recognise only expected non-returned sales |

| Refund Liability | Expected refunds to customers |

| Cost of Sales | Cost of expected non-returned inventory |

| Return Asset | Expected inventory recovery |

This framework allows financial statements to reflect expected customer behavior rather than waiting until returns physically occur.

Example: Expected Returns

Assume:

Return Scenario

| Item | Amount |

|---|---|

| Units Sold | 100 |

| Selling Price | $100 |

| Cost per Unit | $40 |

| Expected Return Rate | 10% |

Expected outcome:

- Revenue recognised = $9,000

- Refund liability = $1,000

- Cost of sales = $3,600

- Return asset = $400

Notice what happened.

Although the company collected $10,000 in cash, only $9,000 is recognised as revenue.

The remaining amount reflects expected future refunds.

Revenue therefore reflects economic reality rather than cash collection.

Loyalty Programmes and Gift Cards

Modern retailers increasingly rely on customer retention programs.

Examples include:

- Airline mileage programs

- Department store reward points

- Coffee shop loyalty cards

- Membership rewards

From an accounting perspective, these benefits are not free.

They create additional obligations.

Common Retail Customer Incentives

| Incentive | Accounting Treatment |

|---|---|

| Loyalty Points | Separate Performance Obligation |

| Membership Rewards | Separate Performance Obligation |

| Gift Cards | Contract Liability |

| Promotional Credits | Variable Consideration Assessment |

A portion of today’s revenue may therefore need to be deferred until the future benefit is provided.

Why Online Retail Is Different

Variable consideration becomes even more important in e-commerce.

Online retailers typically experience:

- Higher return rates

- More frequent promotions

- Greater coupon usage

- Dynamic pricing

As a result, two retailers may report identical gross sales but very different net revenue figures.

This is one reason why comparing online and offline retailers can be misleading without understanding their promotional strategies.

Connecting Back to Part 2

Part 2 focused on identifying the customer.

Part 3 focuses on determining the transaction price.

Once we know who the customer is, we must determine how much revenue the company actually expects to earn.

That amount is not always equal to the sticker price.

Returns, discounts, coupons, loyalty programmes, and gift cards all influence the final revenue number.

The result is that retail revenue becomes a process of estimation rather than simple measurement.

Final Thoughts

Many people assume revenue is an objective number.

In retail accounting, that assumption is often incorrect.

Revenue is frequently an estimate based on expected customer behavior.

Management must forecast returns, evaluate promotional programs, estimate redemption patterns, and determine whether future revenue reversals are likely.

The quality of those estimates directly affects the quality of the financial statements.

This is why retail revenue accounting is not simply about recording sales.

It is about understanding uncertainty.

In Part 4, we will move from accounting estimates to internal controls and audit risks. We will examine how retail companies transform sell-in data into sell-out accounting records and why the month-end adjustment process often becomes the most important risk area in the entire revenue cycle.

Thanks for reading!