Why Retail Revenue Becomes an Audit Risk

Why This Matters

Throughout this series, we have focused on the accounting theory behind retail revenue.

In Part 1, we learned that distribution channels drive accounting outcomes.

In Part 2, we saw that revenue is generally recognised when control transfers to the end consumer.

In Part 3, we discussed how returns, discounts, loyalty programmes, and other forms of variable consideration turn revenue into an estimation exercise.

At this point, a natural question emerges.

How do companies actually convert millions of retail transactions into IFRS-compliant revenue?

The answer is surprisingly simple.

Most retail companies rely on a period-end adjustment process.

And that process often becomes one of the most important risk areas in the entire financial reporting cycle.

The Gap Between Operations and Accounting

Retail businesses generate enormous amounts of transaction data every day.

A typical retailer may process:

- Thousands of daily transactions

- Hundreds of stores

- Multiple sales channels

- Different ERP systems

- Various POS platforms

Operational systems are primarily designed to support:

- Sales activity

- Inventory management

- VAT reporting

- Cash collection

They are not always designed to produce IFRS 15 revenue directly.

As a result, accounting teams often need to perform adjustments at period-end.

Why Adjustments Exist

Recall the concept introduced in Part 1.

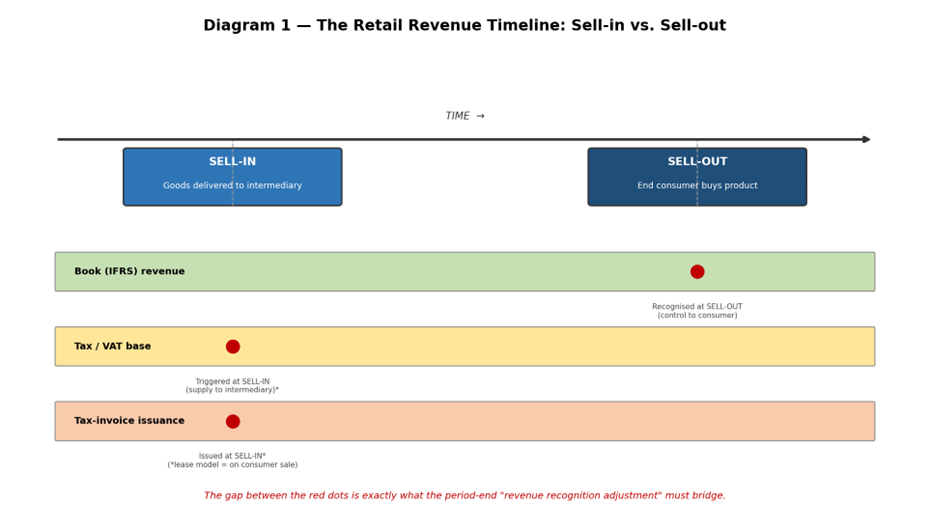

Three Measurement Layers

| Layer | Governing Logic | Trigger Event |

|---|---|---|

| Book Revenue | IFRS 15 | Sell-Out |

| VAT Base | Tax Law | Sell-In |

| Tax Invoice | Tax Law | Sell-In |

Retail systems frequently capture tax events automatically.

Financial reporting, however, follows accounting standards rather than tax rules.

The period-end adjustment exists to bridge this gap.

The Revenue Adjustment Process

At month-end, finance teams typically reconcile transactional records with accounting requirements.

Common Revenue Adjustments

| Channel | Typical Adjustment |

|---|---|

| Consignment | Reverse unsold inventory from revenue |

| Sale-Based Purchase | Recognise consumer sales |

| Agency | Reverse unsold inventory |

| Lease / Concession | Minimal adjustment |

| All Channels | Estimate returns and variable consideration |

The month-end close process converts operational sales data into IFRS-compliant revenue.

Importantly, these adjustments are not corrections of mistakes.

They are a planned component of the accounting process.

Why Auditors Pay Attention

From an audit perspective, retail revenue is unusual.

Individual transactions are generally small.

The systems are often highly automated.

Store-level controls tend to be strong.

Yet revenue remains one of the most important audit areas.

Why?

Because the highest-risk activities are not always found within the transaction systems themselves.

They are often found within the manual adjustments performed after the transactions occur.

Understanding the Risk

Imagine a company reports:

- $500 million of gross sell-in activity

- $30 million of period-end revenue adjustments

If those adjustments are incorrect:

- Revenue may be overstated

- Revenue may be understated

- Inventory balances may be misstated

- Variable consideration estimates may be inaccurate

The accounting standards may be correct.

The ERP system may be functioning properly.

Yet the financial statements can still be wrong if the adjustment process fails.

Where Evidence Comes From

One of the most important audit principles is independent corroboration.

Revenue should not be supported solely by internally generated reports.

Auditors therefore seek evidence from external sources whenever possible.

Typical Sources of Audit Evidence

| Channel | Primary Audit Evidence |

|---|---|

| Consignment | Retailer POS reports |

| Sale-Based Purchase | Consumer sales data |

| Direct Stores | Card settlement reports and bank deposits |

| Wholesale | Tax invoices and customer payments |

| Online | Platform settlement reports |

The objective is simple.

Verify that sales actually occurred.

The Most Important Audit Assertion

When students first learn auditing, they often assume cut-off is the biggest risk in retail.

In practice, the dominant concern is usually occurrence.

Audit Assertions in Retail Revenue

| Assertion | Typical Risk Assessment |

|---|---|

| Occurrence / Existence | High |

| Cut-Off | Moderate |

| Accuracy | Moderate |

| Completeness | Lower |

| Presentation & Disclosure | Lower |

Why occurrence?

Because management generally faces greater incentives to overstate revenue than understate it.

And many of the adjustments discussed earlier have a common characteristic.

They reduce revenue.

A Simple Example

Assume a retailer should record a month-end adjustment reducing revenue by $5 million.

If the adjustment is omitted:

| Item | Correct | Adjustment Omitted |

|---|---|---|

| Revenue | $95 million | $100 million |

| Operating Profit | Lower | Higher |

The omission does not create a complicated accounting error.

It simply causes revenue to remain too high.

This is why auditors devote significant attention to the adjustment process itself.

The Human Factor

Retail systems are increasingly automated.

Month-end adjustments often are not.

Many adjustments still involve:

- Excel calculations

- Manual reconciliations

- Data extraction

- Management estimates

- Review controls

As a result, the greatest risk frequently arises not from technology failures but from human judgment.

The accounting treatment may be theoretically correct while the implementation remains flawed.

Connecting Back to Part 3

Part 3 focused on estimation.

Part 4 focuses on execution.

Knowing how to estimate returns and variable consideration is important.

Applying those estimates consistently and accurately is equally important.

The reliability of retail financial statements therefore depends not only on accounting standards but also on the processes and controls used to implement them.

Final Thoughts

Retail revenue is often viewed as a high-volume, highly automated process.

In reality, some of the most important accounting decisions occur after the transactions have already been recorded.

The journey from sell-in data to IFRS-compliant revenue requires adjustments, reconciliations, estimates, and controls.

That process forms the engine of retail financial reporting.

When the engine operates effectively, financial statements faithfully reflect economic reality.

When it does not, even strong systems and accurate transaction data may fail to produce reliable results.

For auditors, this is why retail revenue remains a significant area of focus.

And for finance professionals, it is a reminder that accounting quality depends as much on process design as it does on accounting theory.

In the final installment of this series, we will step into the shoes of investors and analysts and examine how distribution channels influence reported revenue, margins, and financial statement interpretation.

Thanks for reading!