Hello everyone, this is Global CPA 🙂

Following my previous post comparing IFRS and US GAAP, I thought it would be helpful to organize the overall structure of the USCPA exam itself.

Whenever I prepare for any exam, I personally believe that understanding the overall framework of the test is one of the most important starting points.

First of all, once you pass your first section, you must pass the remaining three sections within 18 months.

Candidates must receive a score of 75 or higher to pass each section.

(Compared to the Korean CPA exam passing score of 60, the cutoff honestly feels higher than many people initially expect )

Unlike many traditional paper-based accounting exams that still exist today, the USCPA adopted the Computer-Based Test (CBT) format as early as 2004.

Personally, before starting the USCPA journey, the only CBT-style exam I had experienced was TOEFL when I was younger, so it definitely took some time for me to adapt to studying and testing entirely on a computer.

Fortunately, once you start practicing consistently with Becker (which I’ll discuss in the next post), you adapt surprisingly quickly .

Many people still consider the USCPA easier than the Korean CPA exam despite the relatively high passing score.

One major reason is the exam format itself.

Unlike the Korean CPA second-stage exam, which heavily emphasizes written calculations and solution processes, the USCPA is largely built around objective testing from a massive question bank.

As long as you can identify the correct answer efficiently, you can cover a huge amount of material.

The exam consists of:

- MCQ (Multiple Choice Questions)

- TBS (Task-Based Simulations)

- WC (Written Communication)

MCQs are standard multiple-choice questions.

TBS questions simulate practical work situations by providing:

- emails

- documents

- exhibits

- accounting data

and asking candidates to solve realistic accounting scenarios.

WC used to exist only in BEC before the CPA Evolution changes introduced in January 2024.

Under the updated exam structure, WC has been removed.

There have also been discussions about the possibility of written communication returning in future revisions, so hopefully everyone preparing now can pass before another major change arrives 😂

One interesting feature unique to CBT exams is the adaptive testing method often referred to as “Item Response Theory.”

The concept is simple:

- candidates who perform well may receive more difficult follow-up questions

- candidates who struggle may receive relatively easier follow-up questions

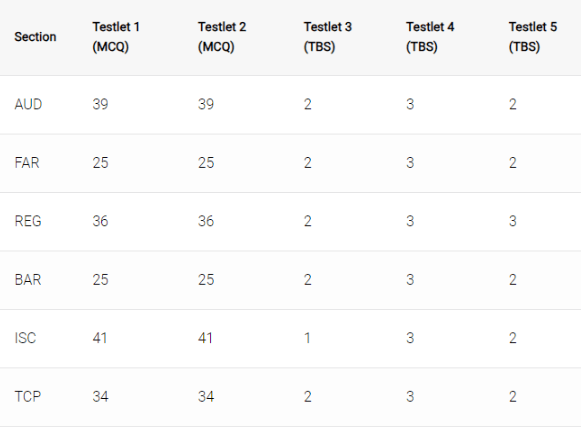

Since the MCQ portion is divided into two separate testlets, if Testlet 2 suddenly feels more difficult after finishing Testlet 1, that is generally considered a positive sign

There are also “pretest questions” included for statistical purposes that do not affect your score at all.

So even if you encounter completely unfamiliar questions during the exam, there is no reason to panic too much.

Honestly, across all four sections, I probably left close to ten questions unsolved… and still passed

USCPA Exam Structure

| Section | Type | Exam Time | MCQ | TBS |

|---|---|---|---|---|

| AUD | Core | 4 hours | 78 (50%) | 7 (50%) |

| FAR | Core | 4 hours | 50 (50%) | 7 (50%) |

| REG | Core | 4 hours | 72 (50%) | 8 (50%) |

| BAR | Discipline | 4 hours | 50 (50%) | 7 (50%) |

| ISC | Discipline | 4 hours | 82 (60%) | 6 (40%) |

| TCP | Discipline | 4 hours | 68 (50%) | 7 (50%) |

The full names of each section are:

- AUD — Audit and Attestation

- FAR — Financial Accounting and Reporting

- REG — Taxation and Regulation

- BAR — Business Analysis and Reporting

- ISC — Information Systems and Controls

- TCP — Tax Compliance and Planning

The three Core sections are mandatory.

Among the three Discipline sections, candidates only choose one.

Back when I took the exam in 2023, these topics were all combined into a single section called BEC, so the structure has changed quite a bit since then.

All exams last four hours.

Candidates can take optional breaks between sections, but only the official 15-minute break after Section 3 does not reduce the remaining exam time.

Every other break continues to consume testing time, so be careful.

Personally, I often felt rushed by the time I reached Testlet 5 in almost every section 😭

So if you are currently preparing, I highly recommend practicing time management during your study sessions as well.

(https://www.aicpa-cima.com/resources/download/learn-what-is-tested-on-the-cpa-exam)

Another important point is that TBS carries enormous weight.

Except for ISC, TBS accounts for at least 50% of the total score.

Since there are relatively few TBS questions, each one carries significant scoring weight.

That is why I believe focusing heavily on TBS practice through Becker is one of the most efficient scoring strategies.

Honestly, the biggest difference between MCQ and TBS is not necessarily complexity.

MCQs directly tell you what the question wants.

TBS requires you to first figure out what the problem is actually asking by reading through materials carefully — very similar to real-world work situations.

As long as:

- your conceptual understanding is solid

- and your reading comprehension is good

TBS becomes much less intimidating over time

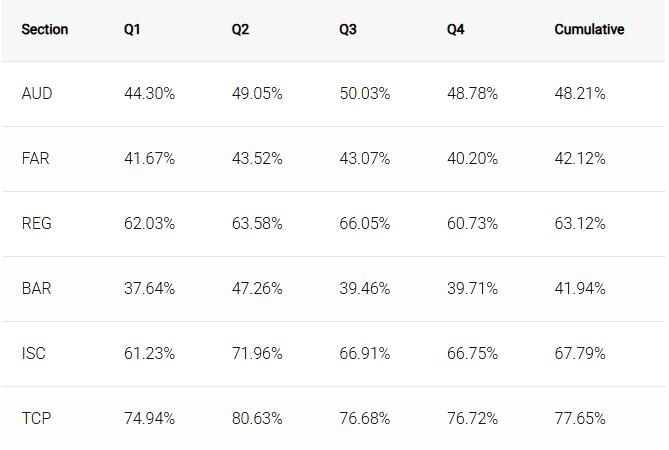

2025 Pass Rates

The 2025 global pass rate statistics showed TCP with the highest overall pass rate among the six sections.

Interestingly, many international candidates — myself included — often find TCP particularly difficult.

One reason the overall pass rate remains high is that many U.S. candidates already have practical familiarity with personal tax filings from everyday life.

Meanwhile, candidates with stronger quantitative and accounting backgrounds often seem to perform relatively well in FAR and BEC-related topics.

Overall, I hope this post helped summarize the overall structure of the USCPA exam:

- exam format

- scoring system

- question types

- section composition

- and pass rates.

Since the CPA Evolution changes after 2024 split the old BEC section into BAR, ISC, and TCP, choosing the right Discipline section has become much more important than before.

In the next post, I’ll break down:

- what each section actually covers in detail

- how the old BEC topics were redistributed

- and how topic weighting works inside each discipline.

All information in this post was summarized based on the official AICPA website and CPA Exam Blueprints.

Thank you again for reading such a long post 🙂

Leave a comment