Hello everyone, Global CPA here ✨✨

In the previous articles, we discussed why companies establish SPCs, how True Sale is evaluated under IFRS, and who ultimately controls an SPC.

Today, let’s take a step back from accounting standards and focus on a more fundamental question.

Why do SPCs issue Senior Debt, Preferred Units, and Common Units instead of simply borrowing money from a bank?

At first glance, the structure may appear unnecessarily complicated. However, each layer exists for a specific reason.

Understanding these layers is essential because they ultimately determine who bears risk, who receives returns, and how the economics of the transaction are distributed.

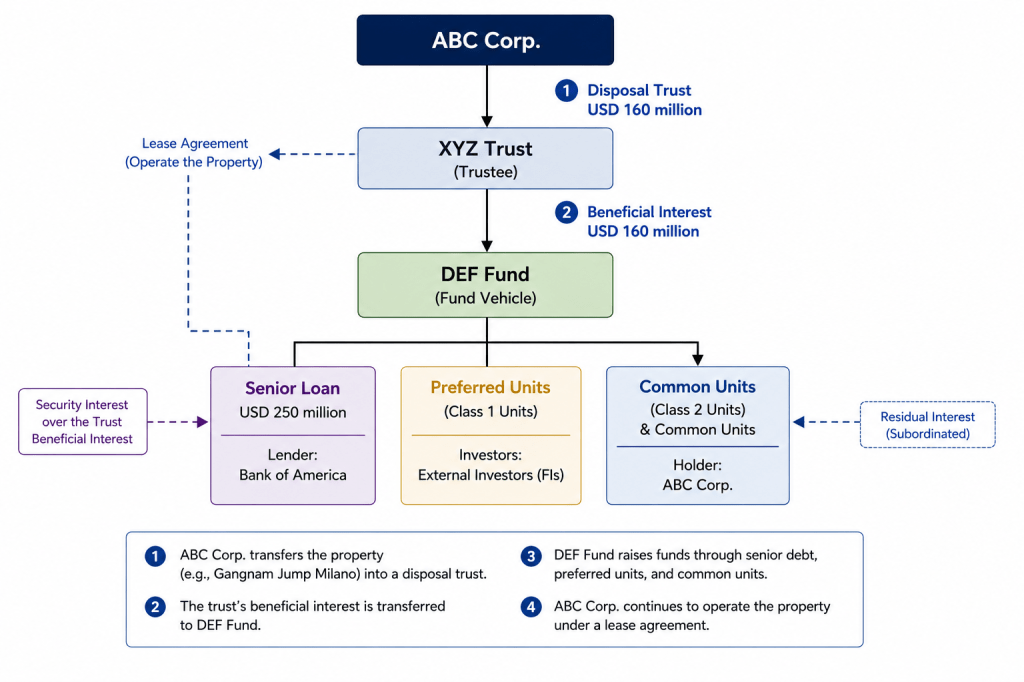

- A Typical SPC Structure

In the above example:

- ABC Corp. transfers a property into a trust structure.

- The beneficial interest is transferred to DEF Fund.

- DEF Fund raises capital through multiple layers of financing.

- ABC Corp. continues to operate the property through a lease arrangement.

At this point, many readers ask:

Why doesn’t DEF Fund simply borrow money from a bank?

The answer lies in one simple concept:

Different investors have different risk appetites.

2. Not All Investors Want the Same Risk

Imagine that you have USD 100 million available to invest.

Some investors prioritize:

- Capital preservation

- Stable income

- Low risk

Others are willing to accept:

- Higher volatility

- Greater uncertainty

- Potentially higher returns

A well-designed SPC allows all of these investors to participate in the same transaction by allocating risks and rewards differently.

This is achieved through a layered capital structure.

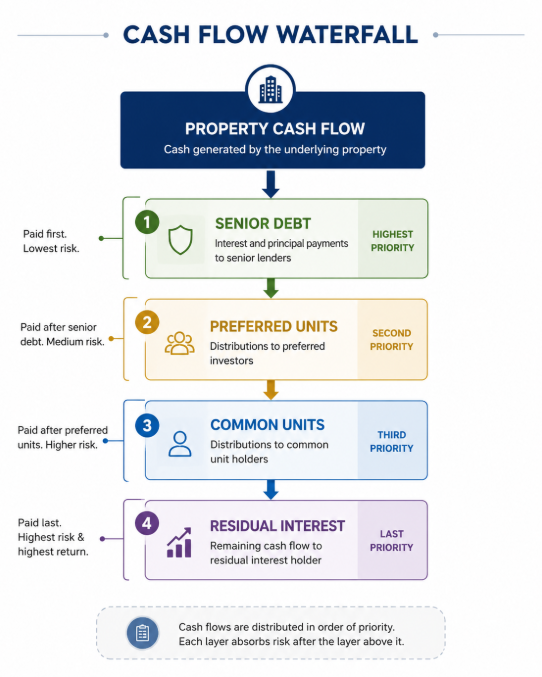

Layer 1: Senior Debt

At the top of the structure sits the senior lender.

In our example, Bank of America provides the senior loan.

Senior lenders enjoy:

- First priority repayment

- Contractual interest payments

- Security interests over the underlying assets

As long as the property generates sufficient cash flow, the senior lender gets paid first.

Characteristics of Senior Debt

Advantages

1) Lowest risk

2) Highest protection

3) Priority claim on cash flows

Disadvantages

1) Limited upside potential

2) Fixed return

Senior lenders are primarily concerned with getting their money back rather than participating in future gains.

Layer 2: Preferred Units

The next layer consists of preferred investors.

These investors accept more risk than senior lenders but receive higher expected returns.

Preferred investors typically receive:

- Fixed or target distributions

- Priority over common investors

- Better yields than senior debt

Think of preferred investors as occupying the middle ground between debt and equity.

They seek:

- Higher returns than lenders

- More protection than equity holders

Layer 3: Common Units

Below the preferred investors sit the common unit holders.

In our example, ABC Corp. retains the common units.

Unlike lenders and preferred investors, common investors do not receive guaranteed returns.

Their performance depends entirely on the success of the transaction.

If the property performs well, common investors benefit.

If performance deteriorates, common investors absorb losses.

As a result, common units carry significantly more risk than senior debt or preferred units.

3. The Most Important Piece: Residual Interest

The residual interest is often the most interesting part of an SPC structure.

After all obligations have been paid:

1) Senior Debt

2) Preferred Investors

3) Common Investors

Any remaining cash flows belong to the residual holder.

In our example, ABC Corp. retains the residual interest.

This means ABC Corp. participates in:

- Property appreciation

- Excess rental income

- Unexpected gains

However, ABC Corp. also bears:

- Property value declines

- Operating underperformance

- Unexpected losses

The residual holder therefore occupies the highest-risk and highest-return position within the structure.

4. Understanding the Cash Flow Waterfall

One of the most important concepts in structured finance is the cash flow waterfall.

Cash generated by the underlying property is distributed according to a predefined order.

This simple waterfall concept explains most SPC capital structures.

5. Why Does the Sponsor Retain Common and Residual Interests?

Many people wonder:

If ABC Corp. sold the property, why does it still retain common units and residual interests?

There are several reasons.

1) Alignment of Interests

External investors want confidence that the sponsor remains committed to the success of the transaction.

Retaining a subordinated position demonstrates that commitment.

2) Funding Efficiency

When sponsors retain part of the risk, lenders and preferred investors are often willing to provide financing at more attractive rates.

3) Participation in Future Upside

Sponsors may still wish to benefit from future appreciation of the underlying asset.

By retaining residual interests, they preserve some exposure to future gains.

6. The Real Purpose of an SPC Capital Structure

The primary purpose of an SPC is not simply to isolate assets.

Rather, it is to redistribute economic risks and rewards among different participants.

Each investor selects the level of risk they are comfortable taking:

| Position | Risk Level | Expected Return |

|---|---|---|

| Senior Debt | Low | Low |

| Preferred Units | Medium | Medium |

| Common Units | High | High |

| Residual Interest | Highest | Highest |

The SPC structure allows all of these investors to coexist within the same transaction.

7. Final Thoughts

At first glance, SPC capital structures can appear overly complicated.

In reality, the underlying logic is straightforward.

Different investors want different combinations of risk and return.

The SPC simply divides economic exposure into separate layers so that each participant can choose the level of risk they are willing to accept.

Understanding these layers is essential because they influence not only financing decisions, but also future accounting analyses involving True Sale, risks and rewards, and consolidation.

Thanks for reading!

Leave a comment