Understanding Control Under IFRS 10

Hello everyone, Global CPA here ✨✨

In the previous article, we discussed one of the most important questions in structured finance:

Does a transfer qualify as a True Sale?

However, even if a transaction passes the True Sale test, another critical question remains:

Who actually controls the SPC?

This question is important because control determines whether the SPC must be consolidated under IFRS 10.

And if consolidation is required, the assets and liabilities inside the SPC may ultimately reappear in the group’s consolidated financial statements.

1. The Common Misunderstanding

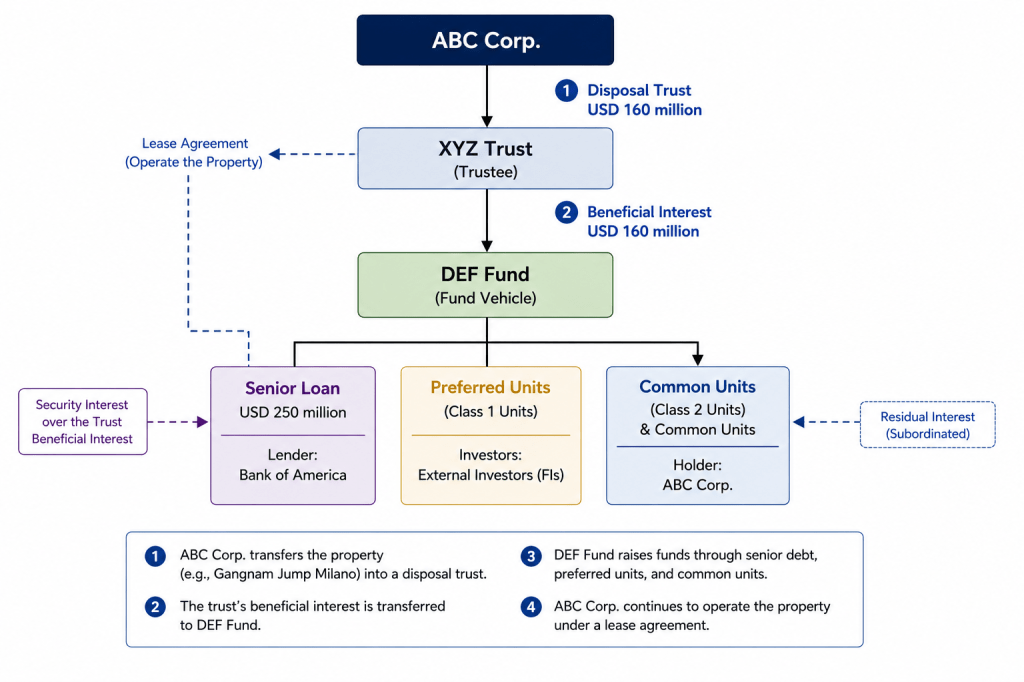

Many people assume that the following structure automatically removes assets from the consolidated balance sheet.

The logic appears straightforward:

- ABC Corp. transfers the property into a trust structure.

- The beneficial interest is transferred to DEF Fund.

- External investors participate through preferred units.

- The SPC becomes a legally separate entity.

At first glance, it appears that ABC Corp. no longer owns the asset.

However, IFRS 10 asks a different question.

Who has control over the relevant activities of the SPC?

2. Legal Ownership Is Not the Same as Control

One of the core principles of IFRS 10 is that legal ownership alone does not determine consolidation.

Instead, control exists when an investor has:

1) Power

The ability to direct relevant activities.

2) Exposure to Variable Returns

The ability to benefit from or suffer from the performance of the SPC.

3) Linkage

The ability to use that power to affect those returns.

All three conditions must be considered together.

Step 1 – Who Has Power?

The first question is:

Who makes the important decisions?

Examples include:

- Sale of the property

- Refinancing decisions

- Tenant selection

- Asset management strategy

- Disposal timing

In many SPC structures, legal ownership may sit with a trustee.

However, if ABC Corp. effectively directs these decisions, power may still remain with the sponsor.

This is often the first warning sign for consolidation.

Step 2 – Who Bears the Upside and Downside?

Next, IFRS examines economic exposure.

Looking at our structure:

- Senior lenders receive fixed interest.

- Preferred investors receive a target return.

- ABC Corp. holds common units and residual interests.

This is important because residual interests usually absorb:

- Remaining profits

- Remaining losses

- Property appreciation

- Property depreciation

In other words:

ABC Corp. may still be exposed to the majority of variable returns.

Step 3 – Can Power Affect Returns?

This is where many structures fail the consolidation analysis.

Suppose ABC Corp.:

- manages the property,

- controls major decisions,

- and retains the residual economics.

In that case, ABC Corp. possesses:

✓ Power

✓ Variable returns

✓ The ability to use power to influence those returns

Under IFRS 10, this combination typically indicates control.

3. Applying IFRS 10 to Our Example

Let’s revisit the structure.

Although:

- legal ownership was transferred to XYZ Trust,

- external investors participate through DEF Fund,

ABC Corp. may still:

- operate the property,

- influence strategic decisions,

- retain residual interests,

- absorb significant economic risks.

If those facts exist, IFRS may conclude that:

ABC Corp. controls the SPC.

As a result:

- DEF Fund may need to be consolidated.

- Assets remain in the consolidated balance sheet.

- Debt raised through the structure may also remain consolidated.

4. Why Many SPCs Are Consolidated

A common misconception is:

“I own less than 50%, so I don’t control it.”

IFRS 10 does not rely solely on voting percentages.

Many SPCs have little or no meaningful voting rights.

Instead, control often depends on:

- contractual arrangements,

- decision-making rights,

- economic exposure,

- and practical ability to direct activities.

This is why many structured entities are consolidated even when ownership percentages appear low.

5. Practical IFRS 10 Checklist

When evaluating an SPC, ask:

Power

✓ Who makes key operating decisions?

✓ Who controls asset disposal?

✓ Who directs cash flow management?

Returns

✓ Who benefits from upside performance?

✓ Who absorbs downside losses?

✓ Who holds residual interests?

Linkage

✓ Can that party use its decision-making power to influence its returns?

If the answer is “Yes” to all three areas, control may exist under IFRS 10.

6. The Relationship Between SPC 03 and SPC 04

A useful way to think about these two analyses is:

SPC 03

Can the asset be derecognized under IFRS 9?

↓

SPC 04

Must the SPC be consolidated under IFRS 10?

Both analyses are required.

Passing one test does not automatically pass the other.

This is why structured finance accounting can become surprisingly complex.

Final Thoughts

When reviewing an SPC structure, accountants should not stop at legal ownership.

Nor should they stop at the True Sale analysis.

The ultimate question is:

Who really controls the economics of the structure?

Because under IFRS 10, control—not legal ownership—determines consolidation.

And in many cases, the answer is not the trustee, the fund, or even the external investors.

It may still be the original sponsor.

Thanks for reading!

Leave a comment