Hello everyone, Global CPA here ✨✨

In the previous articles, we discussed why companies establish SPCs and issue ABCP, as well as the distinction between legal transfer and economic substance.

This naturally leads to one of the most important accounting questions in structured finance:

If a company transfers an asset to an SPC, can it automatically remove that asset from its balance sheet?

Many people assume the answer is yes.

After all, the asset has been legally transferred, ownership has changed, and investors have provided funding.

However, IFRS 9 often reaches a very different conclusion.

1. The Misconception About SPC Transactions

One of the most common misconceptions in structured finance is:

“Once the asset is transferred to an SPC, it disappears from the balance sheet.”

From a legal perspective, this may appear reasonable.

However, accounting focuses on economic substance rather than legal form.

As a result, the key question is not:

Who legally owns the asset?

Instead, IFRS asks:

Who ultimately bears the risks and receives the benefits associated with the asset?

This distinction is the foundation of derecognition accounting.

2. What Is Derecognition?

Derecognition simply means removing an asset or liability from the statement of financial position.

For financial assets, IFRS 9 requires companies to evaluate whether the transfer has genuinely changed the economic position of the parties involved.

The analysis generally follows three key questions:

- Have the contractual rights to the cash flows expired?

- Has the asset been transferred?

- Have the risks and rewards been transferred?

Only after answering these questions can a company determine whether derecognition is appropriate.

Step 1: Have the Contractual Rights Expired?

This is the simplest scenario.

Examples include:

- A trade receivable has been collected.

- A loan has been repaid.

- A bond has matured.

In these situations, the asset ceases to exist and derecognition is straightforward.

Most securitization transactions, however, involve transfers rather than expiration.

Therefore, the analysis continues.

Step 2: Has the Asset Been Transferred?

In many SPC transactions, the answer is yes.

For example:

- Trade receivables are transferred to an SPC.

- Real estate is placed into a trust structure.

- Beneficial interests are sold to investors.

- ABCP is issued based on the transferred assets.

At this stage, many people assume derecognition should occur automatically.

Under IFRS 9, however, the most important analysis has not yet begun.

Step 3: Have the Risks and Rewards Been Transferred?

This is usually the decisive step.

IFRS 9 focuses heavily on whether the company has transferred the significant risks and rewards associated with ownership.

Examples of risks include:

- Credit risk

- Collection risk

- Market value fluctuations

- Residual value risk

- Default risk

If substantially all risks and rewards have been transferred:

→ Derecognition is generally appropriate.

If substantially all risks and rewards have been retained:

→ Derecognition is generally prohibited.

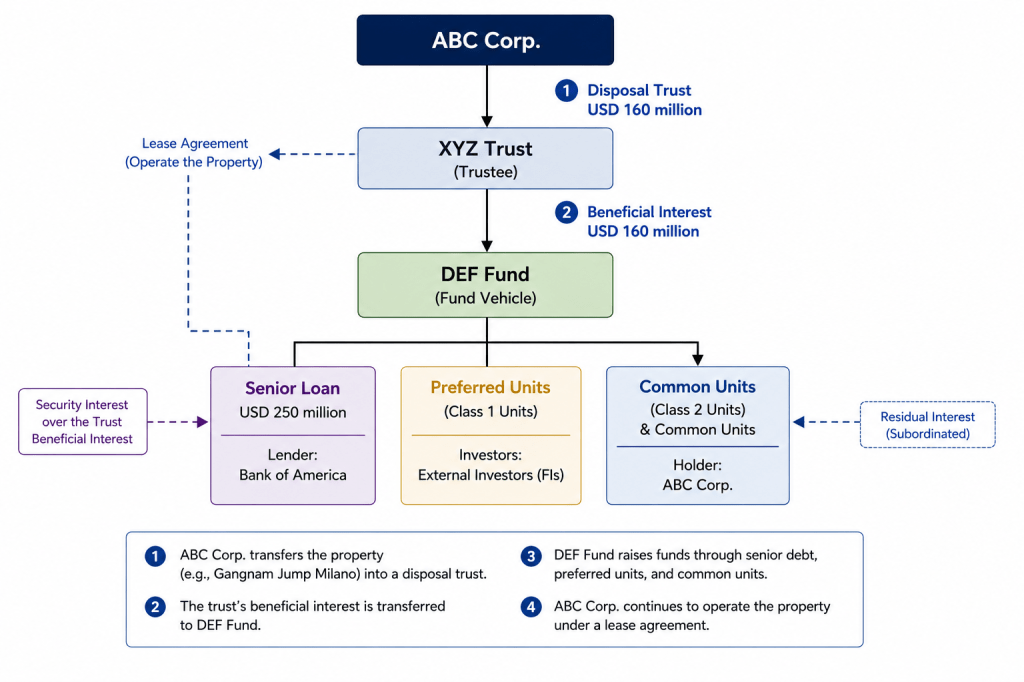

3. A Real-World Example: Property Securitization

Consider a retailer that owns a commercial property.

The retailer places the property into a trust structure and transfers the beneficial interest to an investment fund.

External investors participate in the structure and funding is raised through the capital markets.

At first glance, this appears to be a straightforward sale.

Several indicators support that conclusion:

- The right to receive future proceeds has been transferred.

- Legal ownership has been transferred.

- Investors have provided financing.

Based solely on legal documentation, many would conclude that the asset should be removed from the balance sheet.

However, accounting requires a deeper analysis.

When Economic Exposure Remains

Now assume the retailer continues to:

- Operate the property

- Manage tenants

- Maintain facilities

- Bear repair obligations

- Handle disputes and operational risks

- Influence future disposal decisions

In addition, suppose the retailer continues to participate in future gains from the property while also bearing a significant portion of potential losses.

Although legal ownership has changed, the company continues to maintain substantial economic exposure to the asset.

In substance:

The company may still be carrying many of the same risks it held before the transaction.

This is precisely the type of situation that IFRS 9 was designed to identify.

True Sale vs Financing Transaction

In structured finance, the term True Sale is frequently used.

A True Sale generally implies that:

- ownership has transferred,

- risks and rewards have transferred,

- and the seller no longer maintains significant economic involvement.

However, many transactions satisfy only the first condition.

If the company continues to bear significant risks and rewards, IFRS may conclude that:

the transaction is economically a financing arrangement rather than a sale.

In such cases:

- the asset remains on the balance sheet,

- cash received may be recognized as a liability,

- and the transaction is accounted for similarly to secured borrowing.

This often surprises people who focus only on the legal documentation.

4. Why IFRS Focuses on Substance

Following the global financial crisis, regulators became increasingly concerned about transactions that achieved legal asset transfers while leaving economic risks largely unchanged.

As a result, modern accounting standards place significant emphasis on economic substance.

The objective is simple:

Financial statements should reflect who actually bears the economic consequences of the asset.

Not merely who holds legal title.

5. Practical Derecognition Checklist

When reviewing an SPC transaction, consider the following questions:

Legal Form

✓ Has legal ownership been transferred?

✓ Have contractual cash flow rights been transferred?

Economic Substance

✓ Has the company retained guarantees?

✓ Does the company absorb future losses?

✓ Does the company participate in future gains?

✓ Does the company continue to manage or control the asset?

✓ Would the company still suffer if the asset loses value?

If the answer to several of the substance-based questions is “Yes,” derecognition may not be appropriate under IFRS 9.

6. Final Thoughts

Derecognition is one of the most misunderstood areas of structured finance accounting.

Many transactions appear to be sales from a legal perspective.

However, IFRS asks a much more important question:

Has the company truly transferred the economic substance of the asset?

If risks, rewards, and control remain with the original company, legal ownership alone is not enough.

This is why many securitization transactions that look like asset sales ultimately remain on the balance sheet as financing arrangements.

And once we determine whether the asset should remain on the balance sheet, another critical question emerges:

Even if the asset has been transferred, who actually controls the SPC?

That topic will be covered in the next article.

Thanks for reading!

Leave a comment