From legal transfer to accounting substance under IFRS

Hello Everyone, this is Global CPA✨✨

Today, let’s talk about ABCP structures under IFRS

In structured finance, one of the most important concepts is the separation between the originator company and the transferred assets.

A common structure used for this purpose is the combination of an SPC (Special Purpose Company) and ABCP (Asset-Backed Commercial Paper).

Today, I want to organize the basic structure of ABCP transactions and explain an interesting accounting question:

Why does cash inside an ABCP structure sometimes get classified as a financial asset instead of cash?

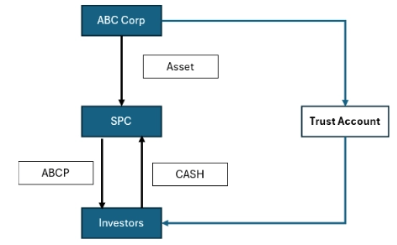

1. Basic Structure of ABCP

An ABCP transaction generally involves four parties:

- Originator company

- SPC (Special Purpose Company)

- Investors

- Trust account / servicing structure

The overall flow looks like this:

- The company transfers assets (receivables, loans, trade receivables, etc.) to the SPC.

- The SPC issues ABCP to investors.

- Investors provide cash to the SPC.

- Cash flows generated from the underlying assets are used to repay investors.

Legally, the assets are usually transferred through a true sale structure, meaning ownership is transferred away from the original company.

Therefore:

- The company no longer has direct legal ownership over the assets.

- The SPC becomes the legal holder of the assets.

- Investors are economically exposed to the cash flows generated by those assets.

2. But Accounting Does Not Stop at Legal Ownership

Under IFRS9, accounting focuses not only on legal form but also on economic substance.

Even if legal ownership is transferred, accountants must still evaluate two critical issues:

(1) Transfer of Risks and Rewards

The key question is:

Has the company truly transferred the economic risks and benefits of the asset?

Examples of retained risks include:

- Credit guarantees

- Repurchase obligations

- First-loss support

- Liquidity support arrangements

If the originator still bears significant economic exposure, derecognition may fail under IFRS 9.

In other words:

Legal transfer alone is not enough.

(2) Control

The second question is whether the company still controls the asset indirectly.

For example:

- Can the company reclaim the asset?

- Can it direct how the asset is managed?

- Does it effectively control the SPC?

If practical control remains, the assets may still remain on the balance sheet.

This is why structured finance accounting often becomes more complex than the legal documentation itself.

3. How Does Cash Move Into the SPC?

There are several common methods for remitting cash into the SPC structure.

| Structure | Description |

|---|---|

| Direct Deposit | Customer → SPC account |

| Indirect Deposit | Customer → Company → SPC |

| Trust-style Structure | Customer → Trust → SPC |

The important issue is not simply where the cash physically sits.

Instead, accountants focus on:

- Who controls the cash?

- Whether the cash is restricted

- Whether the cash can be freely withdrawn

- Whether repayment obligations already exist

In the above example, the transaction is structured using a trust-style arrangement, where cash flows are routed through a trust account before being distributed to investors.

4. Why Is the ABCP Account Sometimes Classified as a Financial Asset Instead of Cash?

This is one of the most interesting accounting issues in securitization structures.

At first glance, the balance inside the ABCP account looks like ordinary cash.

However, under IFRS, not all deposits qualify as “cash and cash equivalents.”

The Core Reason: Restriction and Purpose

Cash generated from the underlying assets continues to flow into the structure.

However:

- The funds are usually reserved for repayment of ABCP investors.

- The company often cannot freely withdraw the balance.

- Usage restrictions exist based on contractual arrangements.

Therefore, although the balance is technically cash in form:

Economically, it behaves more like a restricted financial asset.

5. IFRS Perspective: Cash vs Financial Asset

Under IAS 7, cash and cash equivalents must satisfy characteristics such as:

- Highly liquid

- Readily convertible

- Immediately available for use

- Subject to insignificant risk

But ABCP reserve balances often fail these conditions because:

- Withdrawal restrictions exist

- Funds are trapped inside the securitization structure

- The balance is dedicated to debt repayment

As a result:

- The balance may be classified as a short-term financial instrument

- Or as restricted cash / other financial assets

- Instead of ordinary operating cash

6. Why This Matters in Real Practice

This issue is not merely theoretical.

Classification differences can significantly affect:

- Liquidity ratios

- Net debt calculations

- Credit analysis

- Covenant testing

- Financial statement presentation

Two companies with identical cash balances may look completely different depending on whether the balances are:

- freely usable cash, or

- restricted securitization-related assets.

This is why understanding the economic substance of SPC structures is essential for accountants, auditors, and financial analysts.

Final Thoughts

ABCP structures are a great example of how accounting differs from pure legal interpretation.

Legally:

- ownership may be transferred completely.

But accounting asks deeper questions:

- Who bears the risks?

- Who controls the assets?

- Can the cash actually be used freely?

That difference between legal form and economic substance is at the heart of IFRS-based structured finance accounting.

And once you start studying SPCs and securitization, you realize:

Structured finance accounting is really about tracing economic reality hidden underneath legal contracts.

Thanks for reading.

Leave a comment