Hello everyone, Global CPA here ✨✨

Recently, the overall offline retail industry has been experiencing significant pressure.

Compared with online platforms, traditional retail companies generally operate with much higher fixed costs because they must continuously maintain physical stores, logistics infrastructure, and large workforces.

As a result, offline retailers tend to have higher operating leverage and financial pressure.

When consumer sentiment weakens (especially during periods such as the COVID-19 pandemic) the impact on profitability and cash flows becomes much more severe.

Even after the pandemic, many retailers have struggled to fully recover their sales levels.

This has led to an important trend in the market:

the securitization and monetization of retail properties.

Instead of simply holding stores as long-term operating assets, many companies have started using their real estate as a financing tool.

Why Not Just Borrow Money Traditionally?

At first glance, a retailer needing liquidity could simply:

- sell stores directly, or

- obtain additional bank loans.

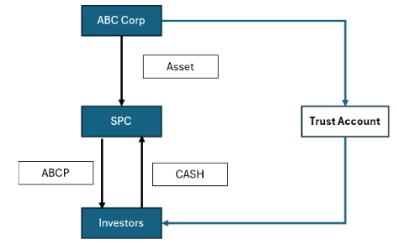

However, many companies instead choose to establish an SPC (Special Purpose Company) and issue ABCP (Asset-Backed Commercial Paper) through a securitization structure.

Because securitization can provide several strategic advantages compared with traditional financing.

1. Liquidity Generation Without Immediate Operational Disruption

One major advantage is that companies can generate liquidity while continuing to operate their business.

For example:

- stores may be transferred into an SPC,

- but the retailer can continue using the properties through lease arrangements or operational agreements.

Economically, the company unlocks cash from its assets without completely abandoning its business operations.

This is especially important for retailers that still need physical locations to maintain brand presence and customer access.

2. Lower Financing Costs

Another important reason is funding efficiency.

When assets are isolated inside an SPC, investors often evaluate:

- the quality of the underlying assets,

- expected cash flows,

- and structural protections,

rather than focusing entirely on the financial condition of the retailer company itself.

This process is commonly referred to as bankruptcy remoteness.

Because the assets inside the SPC are legally separated from the originating company, investors may perceive lower risk, which can reduce financing costs compared with ordinary corporate borrowing.

3. Diversification of Funding Sources

Traditional borrowing heavily depends on:

- bank relationships,

- loan covenants,

- and corporate credit ratings.

However, securitization allows companies to access capital market investors directly through ABCP issuance.

This helps diversify funding channels and improve financial flexibility.

In stressed economic environments, maintaining diversified funding sources can become critically important for survival.

4. Balance Sheet and Financial Ratio Management

Another motivation involves financial reporting and leverage management.

Depending on the transaction structure and IFRS accounting analysis:

- certain assets may qualify for derecognition,

- liabilities may be structured differently,

- and liquidity ratios may improve.

Of course, IFRS does not automatically allow off-balance-sheet treatment simply because assets are transferred legally.

The accounting treatment ultimately depends on whether:

- risks and rewards are transferred,

- control is relinquished,

- and derecognition requirements under IFRS 9 are satisfied.

Still, from a financial management perspective, securitization structures can provide greater flexibility compared with ordinary secured borrowing.

5. Why ABCP?

ABCP is frequently used because it provides short-term funding at relatively efficient market rates.

The structure generally works as follows:

- Assets are transferred into the SPC.

- The SPC issues short-term commercial paper to investors.

- Investors provide funding.

- Cash flows generated from the assets are ultimately used to repay investors.

In many cases, the underlying assets include:

- trade receivables,

- lease receivables,

- credit card receivables,

- or real estate-related cash flows.

As long as investors trust the quality of the underlying assets and the structure itself, ABCP can become an efficient financing tool.

Final Thoughts

The rise of SPC and ABCP structures reflects more than simple accounting engineering.

In many cases, these structures emerge because companies are searching for:

- liquidity,

- funding diversification,

- financial flexibility,

- and survival during difficult economic conditions.

Especially in industries with high fixed costs such as offline retail, securitization can become a powerful financing strategy.

However, once assets and cash flows move into an SPC structure, a much more important accounting question emerges:

Has the company truly transferred the economic substance of the assets under IFRS?

That question will be discussed in the next article:

SPC 02 – Legal Transfer vs Economic Substance Under IFRS

Thanks for reading.

Leave a comment