Why the Customer Is Not Always Who You Think It Is

Why This Matters

In Part 1, we explored how retail companies sell products through different distribution channels.

Whether products are sold through department stores, franchise stores, concession arrangements, or direct-operated stores, the accounting outcome often depends on one fundamental question:

Who is the customer?

At first glance, the answer appears obvious.

If a fashion brand ships products to a department store, isn’t the department store the customer?

If products are delivered to a franchise operator, shouldn’t revenue be recognised at that point?

Interestingly, IFRS 15 often reaches a different conclusion.

To understand why, we need to examine retail revenue through the lens of IFRS 15.

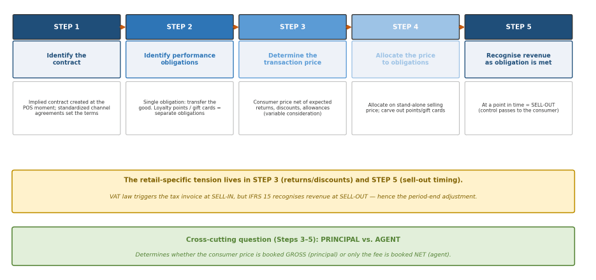

The IFRS 15 Five-Step Model

Revenue recognition under IFRS 15 follows a five-step framework.

Table 1. IFRS 15 Five-Step Model

| Step | Description |

|---|---|

| Step 1 | Identify the Contract |

| Step 2 | Identify Performance Obligations |

| Step 3 | Determine the Transaction Price |

| Step 4 | Allocate the Transaction Price |

| Step 5 | Recognise Revenue |

IFRS 15 requires companies to evaluate contracts, obligations, pricing, allocation, and timing before recognising revenue.

Although the framework applies to all industries, retail companies encounter a unique challenge in Step 1.

Who is the actual customer?

Step 1: Identifying the Customer

For many retail transactions, two parties appear between the brand and the final consumer.

Consider a department store arrangement.

The product moves:

Brand → Department Store → Consumer

At first glance, it may appear that the department store is the customer.

However, accounting is concerned with economic substance rather than legal form.

In many retail arrangements:

- The brand controls pricing.

- The brand bears inventory risk.

- The brand determines promotional activities.

- The brand ultimately earns the economic benefit from the sale.

As a result, the department store often functions as an intermediary rather than the customer.

The economic transaction is therefore:

Brand → Consumer

This distinction explains why many retail companies recognise revenue when products are sold to consumers rather than when products are delivered to retailers.

Step 2: Identifying Performance Obligations

For a typical retail sale, the analysis is relatively straightforward.

Table 2. Common Retail Performance Obligations

| Transaction Type | Performance Obligation |

|---|---|

| Standard Product Sale | Deliver Product |

| Loyalty Programme | Product + Loyalty Points |

| Gift Card | Future Delivery of Product |

| Membership Benefits | Product + Future Services |

Most retail transactions involve a single performance obligation: transferring control of a product.

However, loyalty points, gift cards, and membership programmes may create additional obligations that must be accounted for separately.

We will revisit these items in Part 3.

Step 3: Determining the Transaction Price

At first glance, the transaction price seems easy to determine.

A customer purchases a jacket for $100.

Revenue equals $100.

Simple.

Unfortunately, retail businesses rarely operate under such ideal conditions.

The final amount retained by the company may be affected by:

- Returns

- Coupons

- Rebates

- Promotional discounts

- Loyalty rewards

As a result, retail revenue is often an estimate rather than a fixed amount.

This estimation process is known as variable consideration and represents one of the most important areas of judgment under IFRS 15.

Step 4: Allocating the Transaction Price

For most retail transactions, Step 4 is relatively simple.

A single product is sold for a single price.

No allocation is required.

However, allocation becomes important when multiple performance obligations exist.

Examples include:

- Product + loyalty points

- Product + membership benefits

- Product bundles

In such cases, the transaction price must be allocated based on relative standalone selling prices.

Step 5: Recognising Revenue

This is the step most people associate with revenue recognition.

Revenue is recognised when control transfers to the customer.

Revenue Recognition Trigger

| Event | Typical IFRS 15 Outcome |

|---|---|

| Product Delivered to Department Store | Usually No Revenue |

| Product Purchased by Consumer | Revenue Recognised |

| Product Returned | Revenue Adjusted |

This principle explains the sell-in versus sell-out distinction discussed in Part 1.

Although products may physically leave the warehouse earlier, revenue is generally recognised only when control passes to the end consumer.

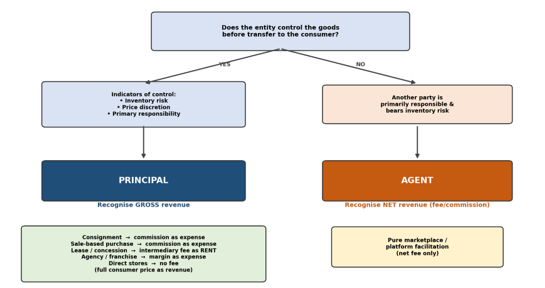

Principal vs Agent

The most important judgment in retail accounting is often not the timing of revenue recognition.

It is determining whether the company acts as a principal or an agent.

| Indicator | Principal | Agent |

|---|---|---|

| Controls Product Before Sale | Yes | No |

| Bears Inventory Risk | Yes | No |

| Controls Pricing | Yes | No |

| Revenue Presentation | Gross | Net |

When a company acts as a principal, revenue is presented on a gross basis.

When a company acts as an agent, only the commission or fee is recognised as revenue.

This single judgment can dramatically change reported revenue, gross margin ratios, and financial statement analysis.

Connecting Back to Part 1

Part 1 introduced the channel map.

Part 2 explains why those channels exist from an accounting perspective.

The key insight is that IFRS 15 focuses on economic substance rather than legal form.

The customer is often the end consumer rather than the intermediary.

The consequence is that revenue is generally recognised at sell-out rather than sell-in.

Once this principle is understood, many of the accounting differences between retail channels become much easier to explain.

Final Thoughts

Retail revenue accounting is often perceived as a question of timing.

In reality, it is first a question of identifying the customer.

Before accountants can determine when revenue should be recognised, they must determine who the revenue is being earned from.

This seemingly simple question drives the entire accounting model.

It influences whether revenue is recognised at sell-in or sell-out, whether revenue is presented on a gross or net basis, and whether intermediaries are treated as customers or merely part of the distribution process.

For that reason, the most important lesson from IFRS 15 is not a journal entry or a paragraph reference.

It is the principle that accounting should reflect economic substance rather than legal form.

In Part 3, we will move from timing to measurement and explore how returns, coupons, discounts, loyalty programmes, and gift cards create the estimation challenges collectively known as variable consideration.

Thanks for reading!

Leave a comment