Why the Same Retail Sale Can Lead to Four Different Accounting Treatments

Why I Started This Series

During my years in audit, I worked with several retail and consumer goods companies.

One of the most interesting observations was that two companies could sell almost identical products to similar customers and yet report revenue in completely different ways.

Some products were sold through department stores.

Others through franchise stores.

Others through company-operated stores, outlets, wholesalers, or online platforms.

At first, I assumed revenue recognition would be relatively straightforward. After all, a customer purchases a product and the company records revenue.

The reality was far more complicated.

The same sale could trigger different journal entries, different VAT treatments, different inventory movements, and different audit procedures depending on the distribution channel involved.

Over time, I realized that understanding retail accounting requires understanding retail operations first.

This series was created to bridge that gap.

Rather than starting with IFRS paragraphs or journal entries, we will start with the business itself: how products move from manufacturers to customers, and why that journey matters from an accounting perspective.

Introduction

Retail revenue often appears deceptively simple.

A customer walks into a store, purchases a product, and leaves with it. Cash is collected, inventory is reduced, and revenue is recognised.

At first glance, there seems to be little room for accounting complexity.

However, the reality inside large retail and consumer goods companies is very different.

A single brand may sell its products through department stores, franchise stores, company-operated stores, online platforms, wholesalers, and concession arrangements simultaneously. Although the customer experiences what appears to be the same transaction, accountants may record each sale differently depending on the distribution channel involved.

This distinction is more than a technical accounting issue. It affects revenue recognition, VAT reporting, inventory accounting, internal controls, audit procedures, and even the way investors interpret financial statements.

Before discussing IFRS 15, journal entries, or audit risks, we must first understand the distribution channels that sit behind retail revenue.

That is the purpose of this article.

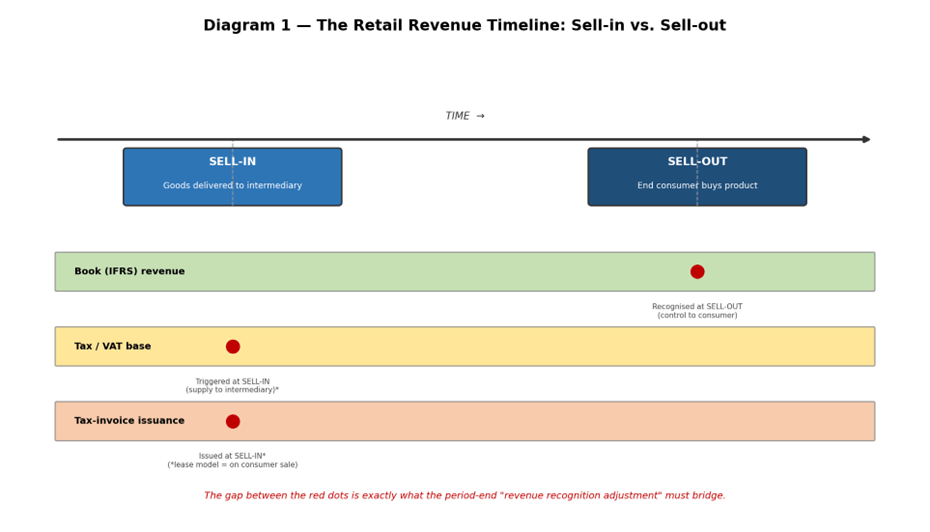

1. Sell-In vs. Sell-Out

The most important concept in retail accounting is the distinction between sell-in and sell-out.

Sell-In

Sell-in occurs when products are delivered to an intermediary.

Examples include:

- Department stores

- Franchise stores

- Retail partners

- Distributors

From an operational perspective, inventory has left the manufacturer’s warehouse and entered the retail network.

Sell-Out

Sell-out occurs when the final consumer purchases the product.

For accounting purposes, this is usually the economically meaningful event because control of the product has transferred to the end customer.

Although the difference appears subtle, it creates one of the most important timing differences in retail accounting.

2. Why Timing Matters

In many retail businesses, accounting records and tax records do not follow the same event.

| Layer | Governing Logic | Triggering Event |

|---|---|---|

| Book Revenue | Accounting Standard (IFRS 15) | Sell-Out |

| VAT Base | Indirect Tax Law | Sell-In |

| Tax Invoice Issuance | Indirect Tax Law | Sell-In (Lease: Consumer Sale) |

As a result:

- Revenue may be recognised on one date.

- VAT may be recognised on another date.

- Tax invoices may be issued on yet another date.

Finance teams therefore spend considerable effort reconciling these different measurement layers during month-end and year-end closing processes.

Understanding this timeline is the foundation for understanding retail accounting.

3. Four Common Retail Distribution Models

Although every retailer has its own business model, most retail transactions can be grouped into four broad categories.

| Channel | When Revenue Is Recognised | VAT Base | Inventory Risk |

|---|---|---|---|

| Consignment | Consumer Sale (Sell-Out) | Supply Amount (Sell-In) | Shared / Substance Depends on Contract |

| Sale-Based Purchase | Consumer Sale (Sell-Out) | Supply Amount (Sell-In) | Brand Owner |

| Lease / Concession | Consumer Sale (Sell-Out) | Consumer Sale | Brand Owner |

| Agency | Consumer Sale (Sell-Out) | Supply Amount (Sell-In) | Depends on Arrangement |

The differences may appear technical, but they directly influence:

- Revenue recognition

- Inventory accounting

- VAT reporting

- Gross margin presentation

- Internal controls

- Audit procedures

For this reason, understanding the channel structure is often more important than understanding the journal entries themselves.

A Real-World Example

Consider a fashion brand such as Zara, Nike, or a local apparel company.

The exact same jacket could be sold through:

- A department store concession

- A franchise store

- A company-operated flagship store

- An online marketplace

From the customer’s perspective, nothing changes.

The customer purchases a jacket.

However, from an accounting perspective, each channel may generate different revenue recognition patterns, different supporting documentation, different VAT treatments, and different internal control considerations.

The economic outcome may be identical, but the accounting presentation can look very different.

This is precisely why retail accounting deserves to be studied at the channel level rather than at the transaction level.

A Simple Example

Throughout this series, we will use a simplified example to illustrate the accounting differences between channels.

Assumptions:

- Selling price: $11,000 (including VAT)

- Net selling price: $10,000

- Quantity supplied: 10 units

- Quantity sold: 7 units

- Cost ratio: 40%

- Retailer margin: 20%

By applying the same numerical example across different channels, we can isolate the accounting impact of each distribution model without introducing unnecessary complexity.

Why the Channel Matters

Many accounting discussions begin with IFRS 15.

In practice, retail accounting begins one step earlier.

It begins with understanding how products reach customers.

A company may sell the same product, at the same price, to the same customer and ultimately generate the same profit.

Yet the accounting presentation can look entirely different depending on whether the transaction occurs through:

- A department store

- A franchise network

- A concession arrangement

- A direct sales channel

The distribution channel acts as the bridge between economic reality and accounting presentation.

Once that bridge is understood, the logic behind revenue recognition becomes significantly easier to understand.

Final Thoughts

At first glance, retail revenue appears straightforward.

A customer buys a product, cash is collected, and revenue is recognised.

However, the reality is far more complex.

Behind every retail transaction lies a distribution channel, and that channel determines how revenue is recorded, how taxes are calculated, how inventory risks are allocated, and ultimately how financial statements are presented.

Two companies may sell exactly the same product to exactly the same customer and generate exactly the same profit, yet report the transaction differently simply because their distribution models are different.

For accountants, auditors, and finance professionals, understanding the channel is therefore the starting point of understanding retail revenue.

Before discussing IFRS 15, journal entries, or audit procedures, we must first understand how products move from the manufacturer to the customer.

That channel map will serve as the foundation for the rest of this series.

In Part 2, we will examine retail revenue through the lens of IFRS 15 and explore why the end consumer—not the intermediary—is usually considered the customer for accounting purposes.

Leave a comment