Hello everyone, this is Global CPA ✨

Welcome back to the USCPA series.

In the previous posts, I organized how to register for the USCPA exam — a foreign professional qualification that is not only administratively complicated, but also significantly more expensive than most domestic exams.

Starting from this post, I wanted to finally organize how I actually studied each section while working full-time.

For the record, I took the sections in the following order:

FAR → BEC → REG → AUD

Before starting, I should mention that this study strategy is mainly intended for candidates who already have some background in:

- accounting

- finance

- or auditing

such as KICPA candidates or working professionals.

Since I was balancing work and study at the same time, my goal was honestly not to study everything perfectly.

Just like I did later with ACCA, my mindset was:

“Let’s pass as efficiently as possible.”

So with that disclaimer out of the way, let’s begin with FAR 🙂

1. Introduction to FAR

FAR is probably the section that corresponds most directly to Financial Accounting in the KICPA curriculum.

FAR stands for:

Financial Accounting and Reporting.

According to the AIFA curriculum structure, FAR can roughly be divided into three major areas:

- Intermediate Accounting

(Financial statement accounts: assets, liabilities, equity, revenue, expenses)

- Advanced Accounting

(Consolidations, equity method, EPS, stock compensation, accounting changes, cash flows, etc.)

- Nonprofit & Governmental Accounting

(Accounting for U.S. governments and nonprofit organizations)

Of course, the USCPA exam pulls questions randomly from a massive question bank, so these categories are not perfectly separated in the actual exam.

But based on:

- various passing experiences I researched

- and my own exam experience

it honestly felt like the exam was distributed relatively evenly across these three areas.

2. Study Period & Why I Chose FAR First

After the semi-annual review season ended around August 2022, I was honestly exhausted.

At that point, I seriously began thinking:

“I need to change something.”

Since accounting and audit work were basically the only professional skills I had developed since university, I started wondering:

“What options actually exist outside Korean accounting firms?”

At the time:

- moving into industry roles felt limited

- tax and deal advisory still felt intimidating

- and I wanted something completely different

That was when I started thinking about working abroad.

And eventually, that thought naturally led me toward the USCPA.

As for why I chose FAR first:

it was simple.

Since this was my first foreign professional exam, I wanted to begin with the section I felt most confident about.

BEC worried me because of the IT topics.

REG terrified me because:

“Korean tax law is already difficult… and now U.S. tax law too?”

AUD also felt intimidating because of PCAOB auditing standards.

So despite:

- U.S. Governmental Accounting

- and unfamiliar US GAAP topics

FAR still felt like the safest starting point.

Study Timeline

My FAR study period was roughly:

Late August 2022 → End of October 2022

Approximately 60 days in total.

Originally, when motivation was at its peak, I planned to study like I did during KICPA preparation:

14 hours a day.

I even booked my FAR exam for mid-October before busy season started again.

But reality quickly corrected those plans 😂

Once I reached the Nonprofit Accounting section near the end of September, I realized there was no way I could finish everything in time.

So I eventually rescheduled and took FAR on November 1, 2022.

During those two months:

- I studied roughly 2 hours before work

- and around 4 hours after work on weekdays

which meant I barely managed to secure around 6 study hours per weekday.

On weekends:

- I slept properly

- recovered physically

- and usually studied around 12 hours.

3. My FAR Study Process

My original thought process looked something like this:

“US GAAP is different from IFRS, right?”

→ “Then I should mainly organize the differences first.”

→ “I should review accounting treatments I forgot.”

→ “What exactly is Nonprofit Accounting…?”

→ “Okay, I definitely need lectures for this.”

→ “Becker has simulated exams. I should solve those before the exam.”

Surprisingly, that rough strategy actually worked fairly well.

Step 1 – Reviewing US GAAP vs IFRS (3 Weeks)

Late August → Mid September

Before even creating my study plan, I had already purchased the full AIFA package.

Still, for Intermediate Accounting and Advanced Accounting, I mostly studied independently using the textbooks without watching lectures.

And honestly, that decision probably saved me.

At the time:

- Intermediate Accounting lectures = 31 lectures

- Advanced Accounting lectures = 58 lectures

- Nonprofit Accounting lectures = 39 lectures

If I had tried to watch every lecture from beginning to end while working full-time, I probably would have spent the entire 60 days just watching videos.

So instead, I focused mainly on:

- differences between IFRS and US GAAP

- reviewing accounting treatments I had forgotten

- consolidating important concepts into summarized notes

That process alone took roughly 3 weeks.

Step 2 – Nonprofit Accounting Lectures (2 Weeks)

Late September → Mid October

I originally tried studying Nonprofit Accounting independently as well…

but quickly realized I had absolutely no idea:

- which topics were important

- and which topics only required basic understanding.

So eventually I gave up and took the AIFA lectures taught by Professor Kim Yong-seok.

Fortunately, I had also studied Governmental Accounting from the same professor during KICPA preparation, so adapting to the lectures itself was not difficult.

I watched lectures at:

1.5x speed

but my personal rule was:

“Do not move on unless I fully understand and organize the concept.”

So realistically, even with 4 study hours after work, I could only finish around 3 lectures per day.

Step 3 – Becker Practice Questions (2 Weeks)

Mid October → October 31

The only major exam I had taken before the USCPA was the KICPA.

And unlike KICPA preparation — where I studied full-time as a student — balancing work and USCPA preparation felt completely different.

By mid-October, my mental state was honestly collapsing 😂

On top of that:

- many clients were located outside Seoul

- commuting alone often took nearly 3 hours per day.

So starting in September, I consistently solved Becker multiple-choice questions during my commute.

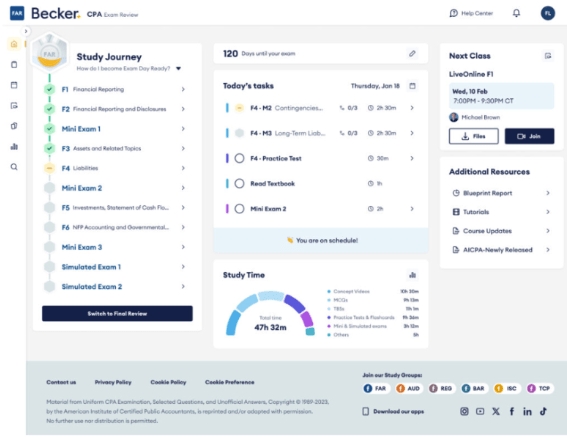

One thing I genuinely loved about Becker was the mobile app.

Since the USCPA heavily emphasizes objective-style questions, solving short MCQs during subway and bus rides turned out to be incredibly efficient.

When I later checked my actual study distribution, I realized:

I had solved far more MCQs during commuting hours than sitting inside study cafés.

Meanwhile, I tried to solve Simulation questions only while sitting down and fully concentrating.

At first, simulations felt intimidating.

But after practicing them repeatedly, I realized they were essentially:

“multiple MCQs connected into one longer scenario.”

So for topics I already felt confident in:

- inventory

- PPE

- revenue recognition

- leases

I actually reduced simulation practice and instead spent more time reviewing Nonprofit Accounting.

Becker Progress & Simulated Exams

Looking back at my Becker progress later, I had only completed around:

40% of the course.

Honestly, seeing that progress bar again now is slightly embarrassing 😂

The lecture completion percentage was also artificially inflated because I sometimes clicked through lectures simply to organize the dashboard.

Most of my actual simulation practice focused on:

- cash flow statements

- equity method

- nonprofit accounting.

I completed both Becker Simulated Exams:

- one two days before the exam

- and the second one the day before the actual exam.

Fortunately, my scores were reasonably good.

That was the moment I finally felt:

“Okay… maybe this study strategy will actually work.”

Final FAR Result

Personally, I’ve always believed that Financial Accounting becomes manageable once:

- you genuinely understand accounting treatments

- and repeatedly practice journal entries by hand.

So instead of solving endless quantities of problems, my strategy focused more on:

- reviewing accounting logic

- understanding unfamiliar nonprofit concepts

- and consolidating important topics efficiently.

Thankfully, that approach worked well for FAR.

Final FAR Score:

89

4. Final Thoughts on FAR

Looking back, the biggest reason I was able to pass FAR in roughly 60 days was probably:

efficient use of fragmented time.

As I mentioned earlier:

- commuting alone probably totaled over 50 hours during September and October.

During that time:

- I solved Becker MCQs

- took screenshots of questions I missed

- and later organized mistakes inside study cafés.

That workflow ended up being surprisingly effective.

Even though the preparation period itself was relatively short, I constantly summarized and condensed materials into one integrated review set before the exam.

5. Comparing FAR with KICPA & ACCA

In terms of conceptual difficulty:

KICPA Financial Accounting (2nd Stage) ≈ ACCA SBR

However, KICPA feels much more difficult psychologically because:

- it is only offered once per year

- and must be taken together with several other subjects simultaneously.

KICPA Financial Accounting (1st Stage) was also significantly harder than ACCA FR in my opinion.

Among all accounting exams I’ve taken, USCPA FAR honestly felt like the easiest financial accounting exam overall.

My personal difficulty ranking would probably look something like:

KICPA Financial Accounting (2nd Stage) >> ACCA SBR >>> KICPA 1st stage > ACCA FR > USCPA FAR

In this post, I organized how I studied FAR — the very first foreign professional exam section I ever attempted.

Looking back now, the period between August and October 2022 still feels strangely emotional.

Balancing work and study during those months was exhausting, but remembering that process again also feels motivating.

In the next post, I’ll return with:

- how I studied BEC

- and how I survived preparing for the exam during busy season in early 2023

Thank you again for reading!!

Leave a comment