Hello Everyone, this is Global CPA✨✨

After sharing my experience with the ACCA FR exam, I wanted to continue with another important part of my ACCA journey — Strategic Business Reporting (SBR).

In this post, I would like to talk about:

- why I chose the International version instead of the UK version,

- how I studied for the exam while working during audit busy season,

- the topics I focused on most heavily,

- and what I learned from the experience.

Why I Chose SBR International Instead of SBR UK

Before discussing my study strategy, I think it is important to explain why I chose the International version of SBR rather than the UK version.

In simple terms, the difference is roughly as follows:

| SBR UK | SBR International |

|---|---|

| Focuses on UK FRS and regulations | Focuses primarily on IFRS |

| Includes UK GAAP and UK company law | Focuses on globally applied standards |

For students planning to work specifically in the UK accounting environment, the UK version may be more appropriate.

However, my long-term interest was broader international accounting rather than UK-specific practice.

Since I also did not have enough time to additionally study UK GAAP during audit season, choosing the International version felt like the most practical decision for me.

One useful thing about ACCA is that the syllabus is updated regularly, and ACCA provides detailed study support resources directly on their website.

Reference:

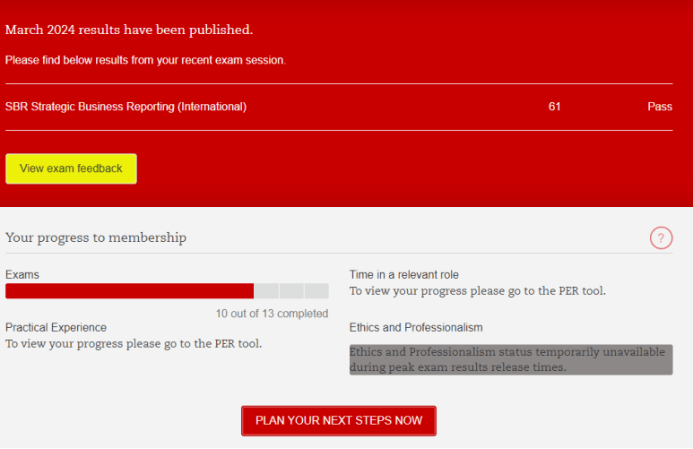

My Result and Overall Study Experience

I passed SBR with a score of 61.

Compared to my FR result, the score was definitely lower, but considering the circumstances, I was honestly satisfied.

At the time:

- Audit busy season was in full swing,

- My available study time was extremely limited,

- and SBR required much more integrated thinking compared to FR.

Unlike FR, SBR is not simply about calculating accounting numbers correctly.

The exam requires candidates to:

- organize information from multiple exhibits,

- understand the reporting objective,

- apply professional judgment,

- and structure responses clearly.

That made the exam much more difficult than I initially expected.

When I first started ACCA, I actually believed FR and SBR would be my strongest subjects because:

- I had already studied KICPA,

- passed the USCPA,

- and worked with IFRS professionally in audit practice.

But once I started solving actual SBR questions, I quickly realized that practical IFRS familiarity and ACCA-style professional reporting are not exactly the same thing.

Structure of the SBR Exam

The SBR exam consists entirely of written-response questions.

The structure is generally:

Section A

- Question 1 (30 marks)

- Question 2 (20 marks)

Section B

- Two questions worth 25 marks each

Unlike the USCPA format, there are no multiple-choice questions.

As someone who was much more comfortable with objective-style exams, this was honestly one of the most intimidating aspects of SBR for me.

The Most Important Topics in SBR

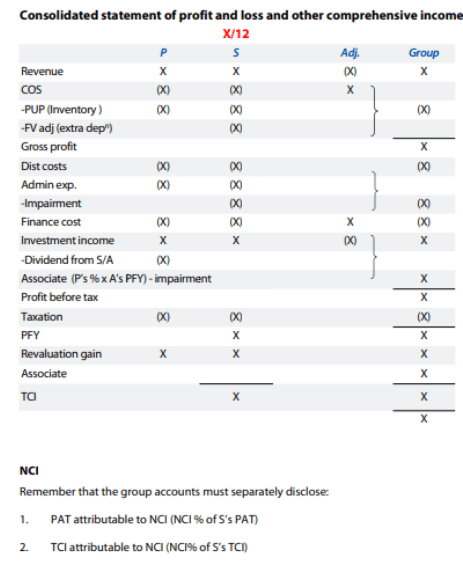

1. Group Financial Statements (Group FS)

If I had to choose the single most important topic in SBR, it would definitely be Group Financial Statements.

This topic appears repeatedly and carries significant weight.

Even though I had worked with consolidated financial statements during audit engagements, solving SBR-style Group FS questions felt very different.

In practice, many consolidation procedures become standardized through templates and systems.

But in SBR, candidates must:

- identify issues from scattered exhibits,

- apply accounting treatments,

- and structure explanations logically.

I strongly recommend practicing Group FS questions repeatedly through past papers.

2. Ethics

Ethics is another extremely important topic in SBR.

In many ways, it is also one of the highest-return topics relative to study time invested.

SBR frequently tests:

- ethical threats,

- professional behavior,

- and the ACCA Code of Ethics.

The Five Fundamental Principles are particularly important:

- Integrity

- Objectivity

- Professional competence and due care

- Confidentiality

- Professional behavior

The various ethical threats also appear frequently:

- Self-interest threat

- Familiarity threat

- Intimidation threat

- Self-review threat

- Advocacy threat

One thing I found helpful was using a structured response framework such as:

“The accountant is facing a familiarity threat, which may impair objectivity under the ACCA Code of Ethics. Therefore, appropriate safeguards should be implemented…”

This kind of structure helped me organize answers more efficiently during the exam.

3. Other Frequently Tested Topics

Some additional areas I encountered frequently while studying included:

- Provisions and contingent liabilities

- IFRS 15 Revenue Recognition

- Operating Segments

- Financial Instruments

- Events after the reporting period

However, if study time is extremely limited, I still believe:

- Group FS

- and Ethics

provide the highest return on investment.

My Actual Study Strategy

My study process was roughly:

- OpenTuition SBR notes

- condensed handwritten summary notebook

- past papers

- Examiner’s Reports

- mock exams

- debriefing lectures

I relied heavily on OpenTuition again because of limited time and efficiency considerations.

One thing I focused on heavily was creating condensed handwritten notes for major financial statement accounts.

For each major account, I summarized:

- definition,

- recognition,

- subsequent measurement,

- and derecognition.

This became surprisingly useful during written-response questions because it gave me a structured conceptual framework I could immediately apply during the exam.

Personally, I think this kind of conceptual organization is especially important in SBR because the subject is fundamentally about professional reporting and judgment.

The Importance of Examiner’s Reports

One of the biggest differences I noticed between ACCA and other qualification systems was the usefulness of Examiner’s Reports.

I spent a great deal of time reading:

- common mistakes,

- weak answer patterns,

- and explanations of what stronger candidates did differently.

Even when I lacked enough time to solve large numbers of past papers, Examiner’s Reports still helped me understand:

- how examiners think,

- what they expect,

- and how marks are actually awarded.

I found this extremely valuable.

Exam Day Reflection

I started organizing SBR concepts in January and began focusing seriously on past papers and Examiner’s Reports during February, which was already peak audit busy season.

Many people recommended Tom Clendon’s SBR lectures, but realistically, I simply did not have enough time for full lecture courses.

Looking back, if I had more time available, I probably would have:

- practiced more mock exams,

- reviewed my answers more deeply,

- and spent additional time strengthening weaker financial reporting areas individually.

Although the score itself was not exceptionally high, passing SBR during audit season taught me something important:

Perfect study conditions rarely exist for working professionals.

Sometimes the goal is simply to continue moving forward consistently despite imperfect circumstances.

Final Thoughts

If I had to summarize my SBR preparation into a few key points, they would be:

- Build strong conceptual understanding first

- Practice Group FS repeatedly

- Memorize and apply Ethics frameworks

- Use Examiner’s Reports aggressively

- Organize concepts into condensed handwritten notes

SBR was significantly more difficult than I initially expected, but it was also one of the most professionally interesting ACCA subjects I have studied so far.

It forced me to think less like a student solving technical questions and more like a professional accountant explaining financial reporting issues to others.

I think that is probably the true purpose of the subject itself.

Thank you for reading.

Leave a comment